Debt is a common financial tool that many people use to achieve their goals. However, not all debt is created equal. Some types of debt can help you build wealth and improve your financial situation, while others can be a burden that holds you back. In this blog post, we will discuss the difference between good and bad debt and how you can use debt to your advantage.

Debt is a common financial tool that many people use to achieve their goals. However, not all debt is created equal. Some types of debt can help you build wealth and improve your financial situation, while others can be a burden that holds you back. In this blog post, we will discuss the difference between good and bad debt and how you can use debt to your advantage.

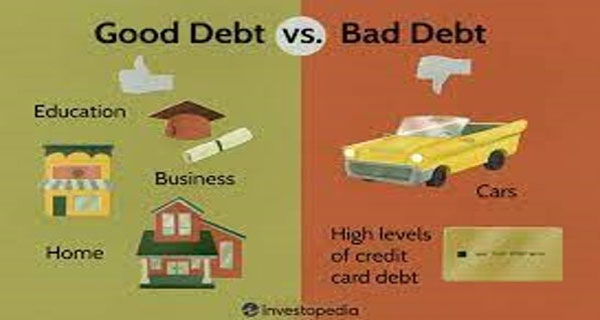

What is good debt?

Good debt is debt that helps you achieve your financial goals and improve your financial situation. This type of debt is usually used to purchase assets that appreciate in value or generate income. Examples of good debt include:

- Mortgages: A mortgage is a loan that is used to purchase a home. Since homes generally appreciate in value over time, a mortgage can be considered good debt. Additionally, owning a home can provide you with a sense of stability and security.

- Student loans: Student loans are used to pay for education expenses. Since education can increase your earning potential, student loans can be considered good debt. However, it’s important to borrow responsibly and avoid taking on more debt than you can afford to repay.

- Business loans: Business loans are used to start or expand a business. Since a successful business can generate income and create wealth, a business loan can be considered good debt.

What is bad debt?

Bad debt is debt that does not help you achieve your financial goals and can be a burden on your finances. This type of debt is usually used to purchase assets that depreciate in value or do not generate income. Examples of bad debt include:

- Credit card debt: Credit card debt is one of the most common types of bad debt. Since credit cards often have high interest rates, carrying a balance on your credit card can be very expensive. Additionally, credit card debt is usually used to purchase consumer goods that do not appreciate in value.

- Payday loans: Payday loans are short-term loans that are used to cover unexpected expenses. However, payday loans often have very high interest rates and can be difficult to repay. Taking out a payday loan can lead to a cycle of debt that is hard to break.

- Car loans: While car loans are not always bad debt, they can become bad debt if you purchase a car that you cannot afford. Since cars depreciate in value over time, taking out a loan to purchase a car can be a burden on your finances.

How to use debt to your advantage

While bad debt can be a burden on your finances, good debt can help you achieve your financial goals. Here are some tips for using debt to your advantage:

- Borrow responsibly: When taking on debt, it’s important to borrow responsibly and avoid taking on more debt than you can afford to repay. Make sure you understand the terms of your loan and have a plan for repaying it.

- Invest in assets that appreciate in value: When taking on debt, consider investing in assets that appreciate in value or generate income. This can help you build wealth and improve your financial situation over time.

- Pay off high-interest debt first: If you have multiple debts, focus on paying off the debt with the highest interest rate first. This can help you save money on interest charges and pay off your debt more quickly.